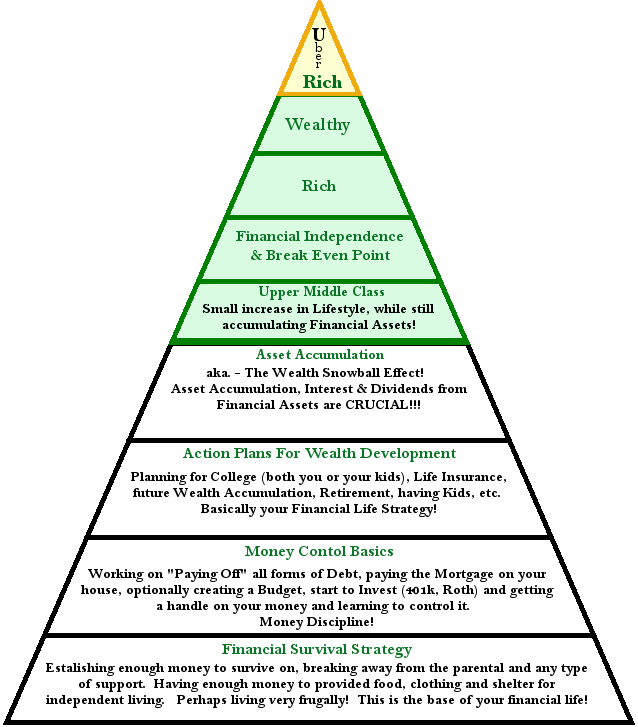

Let’s delve into the financial strategies that differentiate the wealthy from the middle class when it comes to acquiring assets.

- Mindset Shift:

- The wealthy understand that it’s not just about how much money you make; it’s about how you spend it. They prioritize investing in income-producing assets over immediate consumption.

- While the middle class tends to spend any financial windfall on lifestyle upgrades (such as vacations or luxury items), the wealthy focus on building wealth through strategic investments1.

- Income-Producing Assets:

- When the wealthy experience a financial increase (whether from a raise, bonus, or inheritance), they don’t rush to buy toys or liabilities. Instead, they invest in assets that generate income.

- These assets can include real estate properties, dividend-paying stocks, businesses, or other ventures that provide a steady stream of revenue.

- Only after establishing this second income stream do they indulge in luxury purchases1.

- Diversification:

- Wealthy individuals diversify their investments across various asset classes. They allocate resources to stocks, bonds, real estate, private equity, alternative investments, and even start-ups.

- By spreading risk and seizing growth opportunities, they create a robust financial portfolio2.

- Real Estate Investments:

- The wealthy often invest in real estate properties. Owning multiple properties allows them to benefit from rental income and property appreciation.

- In contrast, those with fewer financial means struggle to buy even a primary residence, let alone additional properties3.

- Tax Planning Strategies:

- The rich leverage tax-efficient strategies to minimize their tax burden. They understand the tax implications of their investments and structure their holdings accordingly.

- This includes utilizing tax-advantaged accounts, deductions, and credits to their advantage.

- Professional Financial Advice:

- Wealthy individuals seek guidance from experienced mentors, financially savvy relatives or friends, financial advisors, accountants, and estate planners. They make informed decisions based on expert insights.

- Other less wealthy classes individuals may lack access to financial advice, which can impact their financial choices.

- Retirement Planning:

- The wealthy prioritize retirement planning early on. They contribute to retirement accounts, build pension funds, and create a safety net for their golden years.

- Middle-class individuals often delay retirement planning or rely solely on employer-sponsored plans.

In summary, moving from the middle class to a wealthier class involves having a paycheck and a multiple income streams. The key lies in buying income-producing assets first and indulging in luxury items later. It’s a mindset shift that can transform financial outcomes.

It’s okay to start small, the key is to just start.

MR