After the shock and hit from “The Great Recession”, everybody and their cousins came out and said that the “buy and hold” strategy doesn’t work and the days of 9 to 10% annual returns were over.

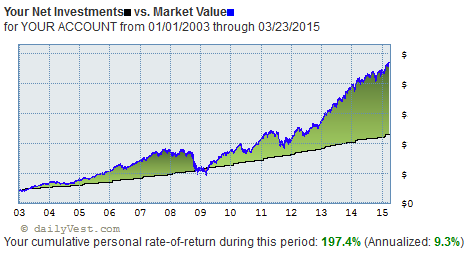

So, I decided to come to the defense of the buy and hold strategy once again. Back in one of my earlier articles called, “Is Buy And Hold Investing Dead“, I stated that I was basically going to stay the course and not deviate much from that philosophy. As a result, I’m happy to say that my Annualized Return is above 9% again (9.3% to be exact). While this number is not quite as great as if it were 10% or slightly higher, I’m still pretty satisfied that it has jumped back up to a normal level.

It’s true, Warren Buffett is definitely not quaking in his boots (I this he averages over 20% annualized), my 401k return is still a decent enough to be satisfied with it. In other articles I mentioned that I wanted to rebalance my portfolio more, but alas I haven’t…

So the chart below is pretty much a Buy and Hold strategy, along with the added benefit of a dollar cost averaging element in place too. While the bull market has been running for quite a while now, I still feel confident enough to say that the basics of a buy and hold strategy has worked well enough for me personally.

Not much more to say, the picture above says it all up to this point. Tomorrow, who knows…

Okay, I’ve noticed a belief going around for the past few years that I feel that I have to write about to dispel the notion that the stock market is broke and not worth participating in!

Both an individual I know, and the media in general has called the past 10 or so years a “lost decade” from an investment standpoint. This is not true, and I’ve been able to achieve over an 8% annual return during the time that the media gurus kept stating that the market has disappointed for the past 10+ years.

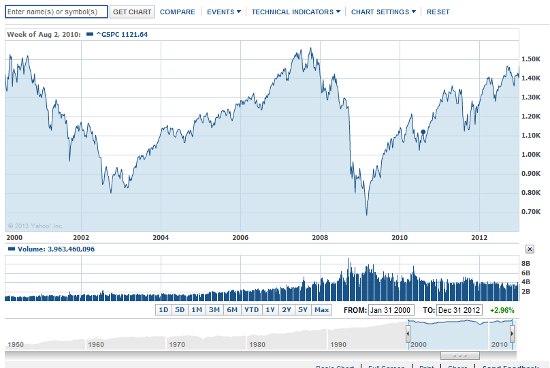

Before I start my explanation as to why they are wrong, let me present the S&P 500 chart for the past 10+ years…

Not pretty huh!

Why You Should Still Invest In The Stock Market

You can see why the media is calling it the “lost decade”… If one were invest all their money all at once (this is called a lump sum) in either year 2000 or at the end of 2007, and not invest any other money, then it’s true, it would have been a lost decade.

But more than likely, you had a 401k plan that would dollar cost average out your contributions during the year. And these stock market dips created an opportunity instead of a flat “lost decade” period of time.

To be honest, my conviction in this “opportunity” was so strong that I increased my contribution amount during the dips that started back in 2008. The amount I increased my contributions was only a few extra percentage points though, so I don’t attribute my over 8% gain to it.

My buddy at work even did better. He’s a young guy and started investing in 2007, and when the 2008 stock market dropped like the bottom fell out, he was discouraged and said he was thinking about stopping his contributions and even pulling his existing money in his 401k (this would have been a huge mistake if he did). I explained to him, the advantages of staying in and told him that I was increasing my contribution amount. Then I explained to him how I was jealous because he was just starting and was going to be able to buy shares of stocks at a huge discount. I even called it a once in a lifetime opportunity. He said I wear rose-colored glasses, and perhaps he’s right, but he didn’t stop contributing and didn’t pull out his money (whew!).

The article on “dollar cost averaging” that I linked to above explains how dollar cost average works, but in case you don’t want to click on it, I’m going to do a quick explanation here.

With an investment instrument like a 401k plan, you buy a set dollar amount of shares of stocks (or really mutual funds) on a repeating periodic basis. In my case that repeating period is every 2 weeks. So when the price of shares of an investment drop in value, I’m able to buy more shares of that investment. This is the magic that enabled me to have an over 8% annual return during the past 10+ years.

To the person not in the know, the past 10+ years in the stock market seem like a tragedy and huge disappointment (aka lost years), but really those dips were great opportunities to buy cheap shares of stocks and mutual funds.

So you will hear people use the chart above to make it sound like the past 10+ years was a huge loss, but really it was a pretty good term, at least in my 401k plan and other stock market investments.

Hope this clears up some confusion as to why it’s still wise to invest in the stock market via a 401k plan.

This past weekend, the blogger Joe at Retireby40 posted an article called: My Overdue Portfolio Checkup, and in the article he states that upon checking out his portfolio fees, they totaled $1,754.91 per year. (Read his article for a great breakdown on his Portfolio Fee Creep, it’s a great read)!

Coincidentally, earlier in the same week, a friend was complaining about the cost of fees in his account. He was complaining because he thought that the .8% that his 401(k) mutual funds were charging was too much. That .8% works out to be $8 per $1,000 invested. While not exactly low, the fees still didn’t spark my brain into calculating my own fees that I pay for the year in my 401k plan. After all, we learn in statistics that anything less than 5% is statistically insignificant (joking here!), and since .8% is less than 1%, it can’t be that bad, right? Wrong!

I figured that Joe had retired, and must have plenty of money to warrant such a hefty fee, and that in my case it wouldn’t really apply. At least that was until I to broke down the costs of my 401(k) fees in my trusty excel spreadsheet! Much to my financial horror, I too, was paying over a thousand dollar in fees! WTF, I haven’t retired and I’m not even close to it in fact!

It was Portfolio Fee Creep! When I started my 401(k) plan, and only have a little invested, the .5%, after all, on a $5,000 balance that fees only work out to be $25 per year, nothing to sweat if the return is good. But now the fees totally over a thousand dollars, I’m pissed! Oh not at the mutual funds companies, no they are not to blame… Instead I’m more upset with my own lack of focus with respect to the operating expense fees. You see, I consider myself a finance guy, and for me to ignore portfolio fee creep is just bad form on my part!

So as Joe has challenged me, I suggest that you check to see what your damage might be from your own portfolio fees too? You might be surprised, I know I was! Oh, and remember… even in a year when your mutual funds lose money, the mutual funds still take their fees out. Talk about adding insult to injury!

On TV and other channels of financial communications, I keep hearing that the “Buy and Hold” strategy is dead or no longer works, but I beg to differ!

The chart above is my 401k balance over the past 8+ years, and as you can tell, my overall balance has almost doubled (97.6 %)! Now granted my 401k investments are in mutual fund which is bit different from buying “blue chip” stocks, but I think most investors do buy and hold mutual funds instead of individual stocks, so hearing such messages adds to the confusion.

Note in the chart above, that the reason I have only 8+ years of data is because that is as far back as I can go with the 401k company that provides information about my 401k balance. If the data went back to 2000, my return would even be higher.

Buy and Hold

Buy and Hold taken as a mindlessly buying and holding stocks without thinking, is not the best approach. But with mutual funds, it’s different! When you buy a mutual fund, there’s (in theory at least) a smart fund managers running the fund for you or an index that weeds out the poorer company performers. So you are paying them to do the thinking/indexing for you.

Buy and Hold Deviations

At my 401k’s core investment philosophy is the “Buy and Hold” strategy! But I have taken some liberties with my 401k account. For instance, during the downturn of “The Great Recession“, my first deviation was that I bumped my 401k contributions to the maximum that was possible. So I was able to buy some shares in the mutual funds in my account at a deep discount (good deal!). This is a stealthy way of buying low (aka timing the market)!

A second deviation from the “Buy and Hold” strategy is that I like to play one of the mutual funds that’s in my account occasionally. By play, I mean trying to buy low and sell high (again timing the market). While this isn’t advisable for most, I know this one particular mutual fund very well! In fact, I know it so well that I’m able fairly accurately guess what direction it takes the majority of the time. This is the wild part of my 401k investment (still very conservative though) and just a very small part of my portfolio that I use to provide a bit of extra interest for myself so that my 401k is more fun for me. This approach probably has raised the overall cumulative value of my entire portfolio by a mere 1 or 2% at the most over these past 8+ years.

Not Following the Herd

During the downturn in 2008, even some of the financial gurus lost faith and were telling people to move to cash. Such a move is very anti-“Buy and Hold” strategy. Perhaps this is why the same group of “financial gurus” say that the “Buy and Hold” strategy is dead?!

I’m not going to mention names, but there were a few highly influential financial gurus that were telling their audience to sell their stocks and other financial investments practically at the market bottom! It was one of the few times in life where I was yelling at the TV (very, very rare), directing my anger at one of the “gurus”, yelling that this was the worst time to move to cash! While the TV guru didn’t heed my advice, I felt better!

Champion investor Warren Buffett believes that the “Buy and Hold” investment strategy still has legs! Perhaps that’s why he is making money instead of providing financial advice… How can the financial community go against the best evidence of a “Buy and Hold” strategy via Buffett when the world’s greatest investor says that it work? Isn’t that kind of telling former boxing champ Mike Tyson that he can’t hit hard and that it’s impossible for him to knock someone out?

Do you think Buy and Hold is dead? What’s your take?

-MR

Did you like this Article? Then please subscribe to my RSS feed so you can check out new articles when they become available. You will help this blog grow by doing so. Thanks!