2020 was horrible in all other respects, except financially!

Better late than never!

Because of the pandemic, I couldn’t work out at the gym and had to stay home which enabled me to gain weight. The company I work for was in the middle of a huge project so many a night, I would be working to 10 pm (sucks considering I start at 6 am), it was rough!

One silver lining was that a bit before February, I started moving a small portion of my investments into cash, but then once the stock market dipped 20% I started moving the cash back into investments in small tranches every few weeks until late May 2020.

Financially, at the end of the year 2020, my return was a few percentage points above what the S&P 500 achieved. So I did okay, I still experienced a big drop in my portfolio value during March and April (which always depresses me a bit), but I held tight, and much like in the past, I increased my contribution percentage. My philosophy during the pandemic was if the fan starts to turn brown and smelled, money wouldn’t really matter much anyway.

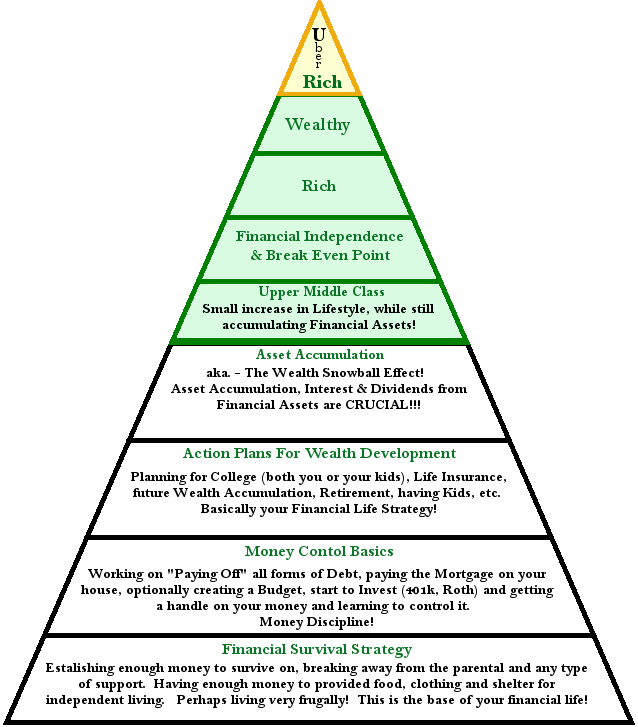

My Financial Pyramid results

So things are moving slowly along. It’s easier to move up from the earlier “white-colored” lower levels than once you get to the “green-colored” levels in the pyramid. Even though financially, I have moved up a quarter in the level called “Upper Middle Class”, I still have a foot firmly at the “Asset Accumulation” level, so I still live pretty frugally. I might go out a bit more than I used to, but I’m still driving a 2010 car, so obviously, my lifestyle has hardly changed.

Grading my performance

My game has improved, and although I’m not quite ready to give myself a solid “A” yet, I’m definitely a higher “A-“. What I could have done better is the following: small investments in crypto and other advanced stock strategies. Actually, there is a lot I would do differently, but that’s another article or two for some other time.

Future Goals climbing the Pyramid

In the next 5 years, I would like to hit the next green level called “Financial Independence and Break-Even Point”. While I couldn’t retire on this level because of future recessions and other market downturns, I would like to semi-retire and get a part-time job, or a hobby job (that makes decent money still). It’s a stretch goal, but we’ll see.

A few of us are thinking about creating a wealth investment club for the less than upper classes (especially blue-collar workers). Half the battle is belief and planning an investment strategy so an investment club with mentors could really help others.

I have had my current investment tragedy for over a decade so I know mistakes I made and I think that my knowledge could benefit others by shortcutting the process for them.

We’ll see, I might wait until I go into semi-retirement to do such a club, but I might start now to work out the bugs with a few people.

We’ll see…